Introduction

Empirical Modal Decomposition (EMD) is an analysis method for non-stationary and non-linear time series which was proposed by

Huang et al, [1998][1]. It is applied in different domains: acoustics, economics, cardiology, biology, turbulence...etc. The method principle is to decompose the time series into a sum of various "modes"

or Intrinsic Mode Functions (IMFs). The EMD is frequently associated to the Hilbert Transform in order to calculate the spectral density for each separated IMF. Before starting with the EMD principle, we introduce the Hilbert spectra analysis. The Hilbert transform of function

:

:

Then, for each mode one can reconstructs the signal such as:

Where

and

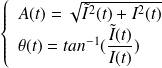

and

represent the amplitude and the phase function respectively, they are defined as:

represent the amplitude and the phase function respectively, they are defined as:

The time series can be reconstructed using the sum of all IMFs: