Conditional distribution of the excesses

The second part of EVT is called the POT method (Peak Over Threshold) consists to use the observations that exceed a certain deterministic threshold and especially the differences between the observations and the threshold, called excess.

Let

a random variable with a CDF

a random variable with a CDF

and

and

which is a real enough large, called threshold. We define the excess over the threshold

the set of random variables

which is a real enough large, called threshold. We define the excess over the threshold

the set of random variables

such as:

such as:

We look from the distribution

of

to define a conditional distribution

of

to define a conditional distribution

with respect to

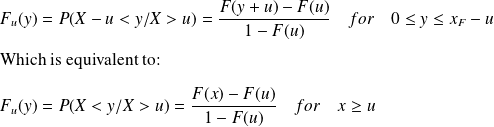

for the random variable exceeding the threshold. We can define the conditional distribution of the excess such as:

with respect to

for the random variable exceeding the threshold. We can define the conditional distribution of the excess such as:

This method allows to determine by which PDF that we can fit the conditional distribution of excesses

when the threshold tends to the point

.

.

Lets

the conditional distribution of cumulative distribution function

with respect to a threshold

. When the threshold

tends to the value

:

The conditional distribution converges to the function

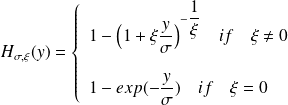

which corresponds to the Generalized Pareto cumulative distribution noted GPD. Generalized Pareto law is written as:

which corresponds to the Generalized Pareto cumulative distribution noted GPD. Generalized Pareto law is written as:

corresponds to Generalized Extreme Value law. For

corresponds to Generalized Extreme Value law. For

(location parameter) the GPD law can be written as:

(location parameter) the GPD law can be written as: